Personal Cloud Storage: How a Once-Niche Utility Became a Pillar of the Global Digital Economy

A Strategic Lens for USA-Update.com Readers

By 2026, personal cloud storage has evolved from a convenient accessory of the internet era into a structural component of the global digital economy, shaping how individuals in the United States and across North America, Europe, Asia, and beyond live, work, travel, and consume information. For the audience of usa-update.com, which closely follows developments in the economy, business, technology, jobs, finance, international relations, and regulation, personal cloud storage is no longer a background technology but an essential lens through which broader market shifts, policy debates, and employment trends can be understood.

The dominance of platforms such as Google Drive, Apple iCloud, Microsoft OneDrive, and Dropbox reflects the convergence of consumer expectations around accessibility, synchronization, and seamless user experience. People now expect instant access to documents, photos, and entertainment content across devices and borders, with data following them as reliably as mobile connectivity or electricity. This expectation extends into professional life, where cloud-based tools underpin remote work, hybrid collaboration, and cross-border project delivery.

For American firms, the personal cloud storage sector has become a showcase of technological leadership and ecosystem design, while simultaneously exposing them to heightened antitrust scrutiny, concerns over privacy and data sovereignty, and intensifying competition from regional champions in Europe and Asia. It is also an increasingly important part of the story of U.S. soft power, as American platforms define digital norms and user habits worldwide, from North America to Europe, Asia, and emerging markets in South America and Africa.

The following analysis, written for publication on usa-update.com, examines how personal cloud storage has developed into an economic engine, an employment driver, a regulatory flashpoint, and a lifestyle infrastructure, and why this market will remain central to discussions about innovation, trust, and competitiveness through the rest of the decade.

From Niche Utility to Everyday Infrastructure

Personal cloud storage began its life as an offshoot of enterprise cloud computing. During the early 2000s, companies such as Amazon Web Services (AWS), Rackspace, and later Microsoft Azure focused on providing scalable infrastructure to businesses rather than individuals. It was only in the late 2000s and early 2010s that the consumer side of the market began to take shape, driven by the insight that the same server capacity used to host corporate data could also provide individuals with reliable, always-on storage.

The turning point came when Dropbox introduced an intuitive drag-and-drop interface and automatic synchronization between devices, lowering the technical barrier for everyday users. This simplicity, combined with generous free storage tiers, transformed cloud storage from an obscure concept into a mainstream service. Shortly thereafter, Google integrated Google Drive with Gmail and later Google Workspace, Apple embedded iCloud into iOS and macOS as the default backup and synchronization backbone, and Microsoft rolled out OneDrive as a natural extension of Windows and Office.

By the mid-2010s, personal cloud storage had become indispensable for students, professionals, and families. The global shift to remote work and remote learning during the COVID-19 pandemic accelerated this dependence, turning the cloud into the de facto repository for critical documents, educational materials, and collaborative projects. According to data from organizations such as the International Telecommunication Union and OECD, the rapid expansion of broadband access and smartphone penetration reinforced this trend across both advanced and emerging economies.

By 2026, personal cloud storage is no longer a standalone product but a deeply integrated layer within broader digital ecosystems, bundled with productivity suites, entertainment subscriptions, smart home platforms, and even financial services. This bundling strategy, visible in offerings like Google One, Apple iCloud+, and Microsoft 365, has turned storage into a retention anchor that keeps consumers inside particular ecosystems, influencing their spending on hardware, software, streaming, and other digital services.

Market Scale, Revenue Models, and Financial Relevance

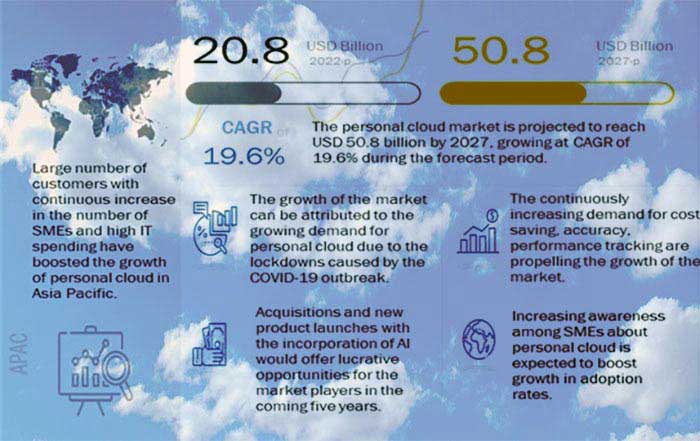

The personal cloud storage market has grown into a substantial and strategically important segment of the global digital economy. Industry research from firms such as Gartner and IDC indicates that global revenue from personal cloud services surpassed the $120 billion mark around 2025 and is on track to approach or exceed $200 billion by the end of this decade, with sustained double-digit compound annual growth rates. This growth is driven not only by rising data volumes but also by the increasing monetization of value-added services layered on top of basic file storage.

The United States remains the epicenter of this market, largely because the leading consumer platforms and most of the major cloud infrastructure providers are American. However, Asia-Pacific markets are now the fastest-growing segment, especially in countries such as India, Indonesia, Vietnam, and Thailand, where rising digital literacy, cheaper mobile data, and smartphone-centric lifestyles have made cloud storage an essential part of the everyday digital toolkit. In China, domestic providers such as Tencent Cloud and Baidu Cloud dominate due to regulatory barriers and data localization mandates, illustrating how geopolitics and regulation can shape market structure.

From a U.S. financial and corporate strategy perspective, personal cloud storage is important not only for direct subscription revenue but also for its indirect contribution to customer lifetime value. A user who pays for extra storage with Google One often remains inside the broader Google ecosystem, adopting services like YouTube Premium, Google Photos, and Nest devices. Similarly, Apple iCloud+ reinforces loyalty to the iPhone, iPad, and Mac hardware ecosystem, while Microsoft OneDrive and Microsoft 365 subscriptions secure long-term relationships with knowledge workers, students, and enterprises.

For readers tracking developments on the finance and business sections of usa-update.com, it is important to recognize that cloud storage revenue is increasingly tied to recurring subscription models. The prevailing freemium structure-offering a small amount of free storage and charging for higher tiers-has normalized monthly payments for digital utilities, in much the same way that streaming services normalized subscriptions for entertainment. Analysts at institutions like the World Economic Forum and McKinsey & Company have noted that this subscription-based digital consumption model is reshaping household budgets and corporate revenue strategies alike.

At the same time, concerns about "subscription fatigue" are growing, particularly in North America and Europe, where households may be juggling payments for multiple streaming platforms, productivity tools, gaming services, and storage plans. This creates pressure on providers to continuously add value-through security features, AI capabilities, or bundled services-to justify recurring fees and reduce churn.

On the investment side, venture capital and private equity continue to target specialized cloud storage startups, particularly those focused on privacy-first offerings, decentralized architectures, or AI-driven organization. However, the market is also undergoing consolidation, as larger players acquire niche providers or integrate their functionality into broader platforms. This dual dynamic-innovation at the edges and consolidation at the core-will remain a defining feature of the sector's financial landscape.

Technology Foundations: AI, Security, and Infrastructure

The personal cloud storage market in 2026 is shaped by a combination of maturing infrastructure and rapid innovation. Several technological trends are central to its evolution and to its broader impact on the economy and employment, themes regularly covered across technology and employment reporting on usa-update.com.

One of the most visible shifts is the integration of artificial intelligence into storage platforms. AI now underpins advanced search, automatic organization, content recommendations, and productivity enhancements. Services like Google Drive and Microsoft OneDrive use natural language processing to allow users to search for files based on context rather than exact file names, while AI-driven tagging of photos and videos helps individuals and families manage rapidly expanding media libraries. Features such as automatic transcription of audio and video, intelligent summarization of documents, and predictive file suggestions are increasingly common and are becoming key differentiators between premium and basic plans. Readers interested in the broader AI landscape can explore resources such as OpenAI and NVIDIA's AI research pages to understand how these technologies are evolving.

Security is another foundational area where personal cloud storage providers are investing heavily. With ransomware attacks, identity theft, and data breaches frequently making headlines on news platforms and global outlets like BBC News and Reuters, consumers and regulators have raised expectations for encryption, authentication, and incident response. Many leading providers are adopting zero-trust security models, where every access request is verified regardless of its origin, and multi-factor authentication-including biometrics-is becoming standard. Apple iCloud+, Dropbox Vault, and privacy-focused services like Proton Drive highlight how encryption and privacy assurances are now central to brand positioning and consumer trust.

Beneath the user-facing features lies a global network of data centers, undersea cables, and edge computing nodes that make personal cloud services possible. Hyperscale data centers operated by Google, Microsoft, Amazon, and others span North America, Europe, Asia, and increasingly regions such as South America and Africa, where digital demand is accelerating. For readers following energy and sustainability issues on energy and global platforms like the International Energy Agency, it is significant that data centers are now major consumers of electricity and a focal point in discussions about digital infrastructure's carbon footprint. Providers are investing in renewable energy, advanced cooling technologies, and more efficient chips to mitigate environmental impact and align with corporate climate commitments.

Edge computing-processing data closer to where it is generated-is also influencing personal cloud storage. By caching frequently used files on local devices or nearby servers while maintaining synchronized backups in the cloud, providers can reduce latency and improve reliability, which is particularly important for mobile-first users in markets like India, Brazil, and South Africa. At the same time, decentralized storage models based on blockchain, such as those promoted by Filecoin and Storj, are testing alternative architectures that distribute data across global networks of independent nodes. While still niche, these models speak to a growing interest in user control and resilience against centralized outages or geopolitical disruptions.

Personal Cloud Storage Evolution

From Niche Utility to Global Digital Infrastructure (2000-2026)

Consumer Behavior, Lifestyle, and Entertainment

For readers of usa-update.com who are as interested in lifestyle and entertainment as in macroeconomic trends, personal cloud storage is increasingly visible in everyday routines. It has become the invisible infrastructure behind photo libraries, streaming experiences, and digital collaboration among families and friends.

In households across the United States, Canada, the United Kingdom, Germany, and other advanced economies, services like Google Photos and Apple iCloud Photos have replaced physical albums and local hard drives as the primary repositories of personal memories. Parents share albums of school events, vacations, and milestones with relatives in Europe, Asia, or Australia, while secure cloud folders store sensitive documents such as medical records, insurance policies, and legal contracts. This shift has changed expectations around data durability; consumers now assume that their digital lives will be preserved indefinitely in the cloud, accessible from any device.

In education, from U.S. high schools to universities in Europe, Asia, and Oceania, cloud storage has become a standard tool, often integrated into institutional platforms. Students use OneDrive or Google Drive to collaborate on group projects, submit assignments, and manage research materials. The normalization of hybrid learning models since the pandemic means that even in-person courses often rely on cloud-based repositories for lecture notes, recorded sessions, and supplemental resources. Organizations such as UNESCO have highlighted how cloud-based tools contribute to digital inclusion and lifelong learning, particularly when combined with affordable mobile devices.

The rise of the gig economy and remote freelancing has also deepened reliance on personal cloud storage. Designers, writers, consultants, and software developers in cities such as New York, Los Angeles, London, Berlin, Singapore, and Sydney routinely use Dropbox, Google Workspace, and Microsoft 365 to share large files, manage client deliverables, and maintain version control. This has created new expectations for reliability, uptime, and cross-border accessibility, reinforcing the strategic importance of global cloud infrastructure.

Entertainment consumption is similarly intertwined with cloud storage, even when users do not think of it in those terms. Streaming platforms such as Netflix, Disney+, Amazon Prime Video, and Spotify rely on cloud architectures to deliver content, while personal storage integrates with these ecosystems for offline downloads, playlists, and personal media libraries. The boundary between personal and platform-managed storage is blurring, as consumers increasingly expect all digital content-whether self-created or licensed-to be available anywhere, anytime.

At the same time, a subset of consumers has become more privacy-conscious, partly in response to high-profile data breaches and surveillance debates covered by outlets like The New York Times and The Wall Street Journal. These users gravitate toward services that emphasize end-to-end encryption, transparent data policies, and jurisdictional protections, such as those in Switzerland or the European Union. This segment may be small in absolute terms but exerts disproportionate influence on policy discussions and on the development of privacy-preserving technologies.

Regulation, Data Sovereignty, and International Tensions

The regulatory environment surrounding personal cloud storage has grown more complex and consequential, particularly for American companies operating globally. For readers of usa-update.com interested in regulation and international affairs, this is an area where technology, law, and geopolitics intersect in ways that directly affect business models and strategic planning.

In Europe, the General Data Protection Regulation (GDPR) remains the cornerstone of data protection law, influencing not only EU-based providers but any company serving European residents. Since its implementation, GDPR has required clear consent mechanisms, data portability, and strict rules on cross-border data transfers. In recent years, European authorities and courts have further tightened requirements around data transfers to the United States, prompting firms to localize more data within EU borders and to adopt new legal frameworks for transatlantic data flows. The European Commission and national regulators continue to refine guidance on AI and automated decision-making, directly affecting how cloud providers can use data for personalization and analytics.

In Asia, data localization laws and digital sovereignty strategies have created a fragmented regulatory map. China's regulatory environment strongly favors domestic providers like Tencent Cloud and Baidu Cloud, limiting the scope for U.S. firms to operate independently. India has moved toward stricter control over cross-border data flows, especially in sensitive sectors such as finance and health, compelling global providers to invest in local infrastructure and partnerships. Countries like Indonesia, Vietnam, and Malaysia are implementing or considering similar rules, often framed as measures to enhance national security, protect citizens' privacy, and foster domestic digital industries.

In the United States, regulatory attention has focused on antitrust issues and platform power. Lawmakers and agencies such as the Federal Trade Commission (FTC) and the Department of Justice (DOJ) have scrutinized whether firms like Google, Apple, Microsoft, and Amazon are leveraging their dominance in operating systems, app stores, or enterprise cloud to entrench their positions in personal storage. Questions about tying practices, default settings, and interoperability are central to these debates, which are closely watched by business leaders and investors who follow news and analysis on usa-update.com and global outlets like Bloomberg.

National security concerns also shape policy. Governments in the United States, Europe, and allied countries are increasingly attentive to where data is stored, who controls the infrastructure, and how law enforcement and intelligence agencies can access information under legal frameworks. This has prompted calls for greater transparency from cloud providers regarding government data requests, as well as investments in secure, sovereign cloud solutions for sensitive public-sector workloads.

The cumulative effect of these regulatory and geopolitical pressures is a shift away from a single, unified global cloud toward a more segmented landscape. Providers must navigate a patchwork of rules, often replicating infrastructure or customizing services for specific jurisdictions. For consumers and businesses, this can mean differences in available features, performance, and legal protections depending on where they are located.

Employment, Skills, and the Cloud-Driven Labor Market

The expansion of personal cloud storage has significant implications for employment and skills, both in the United States and internationally. For readers who follow jobs and employment trends on usa-update.com, the sector offers a useful case study of how digital infrastructure can create new roles across the skill spectrum.

At the high-skill end, demand for cloud architects, software engineers, AI specialists, and cybersecurity professionals continues to exceed supply. Organizations such as the U.S. Bureau of Labor Statistics and CompTIA have documented strong growth in cloud-related roles, with competitive salaries and opportunities in major technology hubs like Silicon Valley, Seattle, Austin, Toronto, London, Berlin, Singapore, and Sydney. Expertise in platforms such as AWS, Azure, and Google Cloud Platform, as well as familiarity with security frameworks and compliance standards, has become a valuable asset for professionals seeking advancement or career transitions.

Cybersecurity, in particular, has emerged as a critical field, as the integrity and availability of personal data are central to consumer trust in cloud services. Roles in threat analysis, incident response, encryption design, and security architecture are expanding across both providers and customer organizations. High-profile security incidents regularly covered by outlets such as Krebs on Security reinforce the perception that robust protection is not optional but a core requirement.

Legal, regulatory, and policy roles have also grown in importance. Multinational cloud providers require teams of privacy officers, compliance managers, and legal counsel who understand the intricacies of GDPR, the California Consumer Privacy Act (CCPA), and data localization laws in Asia and Latin America. This has created new career paths at the intersection of law, technology, and governance, both within corporations and in government agencies tasked with oversight.

Beyond white-collar roles, the construction, operation, and maintenance of data centers generate employment in regions where large facilities are built. States such as Virginia, Ohio, and Texas have attracted significant data center investment, creating blue-collar jobs in construction, electrical work, cooling system management, and physical security. These roles, while less visible than software engineering positions, are essential to the functioning of the digital economy and contribute to local tax bases and infrastructure development.

For workers and job seekers, the growth of personal cloud storage underscores the value of digital literacy and cloud fluency across professions, not only in IT but also in fields such as education, healthcare, media, and finance. As more organizations adopt cloud-native workflows, the ability to manage, share, and secure digital information has become a baseline expectation rather than a specialized skill.

Regional Dynamics: North America, Europe, Asia, and Beyond

The personal cloud storage market reflects regional differences in regulation, consumer preferences, and industrial policy, making it a useful lens for understanding broader international competition and cooperation.

In North America, the United States remains the principal innovation hub, home to Google, Apple, Microsoft, Amazon, and Dropbox, which collectively set global benchmarks for functionality, design, and integration. Canada, with its strong research institutions and privacy-conscious regulatory environment, positions itself as a complementary market that encourages innovation while emphasizing consumer protection.

Europe has carved out a distinctive path centered on privacy, data sovereignty, and open-source alternatives. Initiatives like Nextcloud, headquartered in Germany, provide self-hosted and sovereign cloud solutions for governments and enterprises wary of dependence on U.S. or Chinese providers. European policymakers, through bodies like the European Data Protection Board, continue to push for frameworks that give individuals greater control over their data, influencing how global providers design consent, transparency, and portability features.

Asia presents a mosaic of approaches. China's market is dominated by domestic champions such as Tencent and Baidu, embedded within broader "super-app" ecosystems that integrate messaging, payments, entertainment, and storage. In India, telecom operators partner with global and local providers to bundle cloud storage with mobile data plans, making it more accessible to a vast, mobile-first population. Southeast Asian markets, including Indonesia, Malaysia, Thailand, and Vietnam, are experiencing rapid adoption as digital services expand and middle classes grow. Singapore, with its robust digital infrastructure and pro-business environment, functions as a regional hub for cloud operations.

South America and Africa, while at earlier stages of market development, are seeing accelerated adoption due to smartphone penetration and improvements in connectivity. In Brazil, South Africa, Kenya, and Nigeria, for example, cloud storage is often accessed through affordable mobile packages and integrated with messaging and social media platforms. This mobile-first trajectory allows many users to bypass traditional PC-based computing, reinforcing the centrality of cloud services in digital inclusion.

Australia and New Zealand, with advanced broadband infrastructure and close economic ties to both North America and Asia, serve as important testbeds for new services and regulatory approaches, often adopting hybrid strategies that balance privacy, innovation, and interoperability.

Strategic Outlook to 2030: Trust, Innovation, and Fragmentation

Looking ahead to 2030, the trajectory of personal cloud storage will be shaped by three overarching themes that are highly relevant to the business, policy, and consumer audiences of usa-update.com: trust, innovation, and fragmentation.

Trust will remain the decisive factor in adoption and retention. Providers that can convincingly demonstrate robust security, transparent data practices, and responsible AI use will be better positioned to maintain customer loyalty in a world of increasing digital risk. This includes preparing for emerging threats such as quantum computing, which could undermine current encryption methods, and developing "post-quantum" cryptographic standards in collaboration with organizations like the National Institute of Standards and Technology.

Innovation will continue to transform what personal cloud storage means in practice. The integration of AI will likely turn cloud services into proactive digital assistants that anticipate user needs, summarize and organize content automatically, and integrate seamlessly with other aspects of digital life, from smart homes to connected vehicles and digital identity systems. As governments and businesses explore digital identity and e-government platforms, personal cloud accounts may become central repositories for official documents, health records, and financial credentials, raising both convenience and ethical questions.

Fragmentation, driven by regulation and geopolitics, will challenge the notion of a single, globally uniform cloud. Data localization, national security concerns, and industrial policy will push providers to create region-specific architectures and service configurations. This may increase costs and complexity but also create opportunities for regional players and specialized solutions. For multinational corporations, navigating this fragmented environment will require sophisticated compliance strategies and diversified infrastructure.

For the United States, the personal cloud storage market is both an asset and a test. It showcases the country's capacity for technological innovation and global platform building, but it also exposes American firms to antitrust scrutiny, international regulatory pushback, and competition from state-backed or regionally favored rivals. How U.S. policymakers, regulators, and companies respond to these challenges will influence not only the future of cloud storage but also the broader standing of the United States in the digital economy.

Conclusion: A Cornerstone of the Digital Economy for USA-Update.com Readers

By 2026, personal cloud storage has clearly moved beyond its origins as a convenient file backup solution to become a foundational element of the global digital infrastructure. It underpins remote work, hybrid education, cross-border collaboration, digital entertainment, and everyday lifestyle choices in the United States, North America, and around the world. For the readership of usa-update.com, which closely follows developments in economy, jobs, finance, technology, international relations, and lifestyle, understanding this market is essential to understanding the broader digital transformation.

The sector's continued growth will depend on its ability to balance innovation with responsibility, convenience with privacy, and global reach with respect for local laws and values. Whether through the dominance of U.S.-based giants like Google, Apple, Microsoft, and Amazon, the assertiveness of European privacy frameworks, or the dynamism of Asian super-app ecosystems, personal cloud storage will remain a central battleground for economic influence, regulatory philosophy, and technological leadership.

As usa-update.com continues to cover developments across news, business, technology, international, travel, and related domains, personal cloud storage will feature not only as a technology topic but as a recurring theme in stories about growth, competition, consumer behavior, and the evolving nature of work and life in a fully digital economy.